The Chinese economy is slowing down, but wealthy shoppers in China are still confident about buying luxury goods in 2019. At least that’s what a report published on January 15 by the public relations company Ruder Finn in collaboration with Consumer Search Group (CSG) Hong Kong found. But, the report warns, luxury brands will have to stay on top of fashion trends, keep being innovative, and provide a seamless online/offline shopping experience to win over consumers in 2019, as customer loyalty continues to diminish. And some of the strategies brands are trying right now, the experts warn, aren’t ones that will work.

The report, titled “The 2019 China Luxury Forecast,” is based on a survey of 1,385 consumers across mainland China and Hong Kong. Survey respondents included 1,075 consumers in over 130 cities in China as well as 310 consumers in the Hong Kong Special Administrative Region. Among those surveyed, the average annual household income is 206,740 (RMB 1,400,930) in mainland China and 124,340 (HK975,286) in Hong Kong.

This week, Jing Daily sat down with the report’s authors – Gao Ming (GM), Senior Vice President and General Manager Luxury Practice China of Ruder Finn Asia, and Simon Tye (ST), Executive Director of CSG Hong Kong, to deep dive into some of the findings on innovation and omnichannel retail strategies from the report.

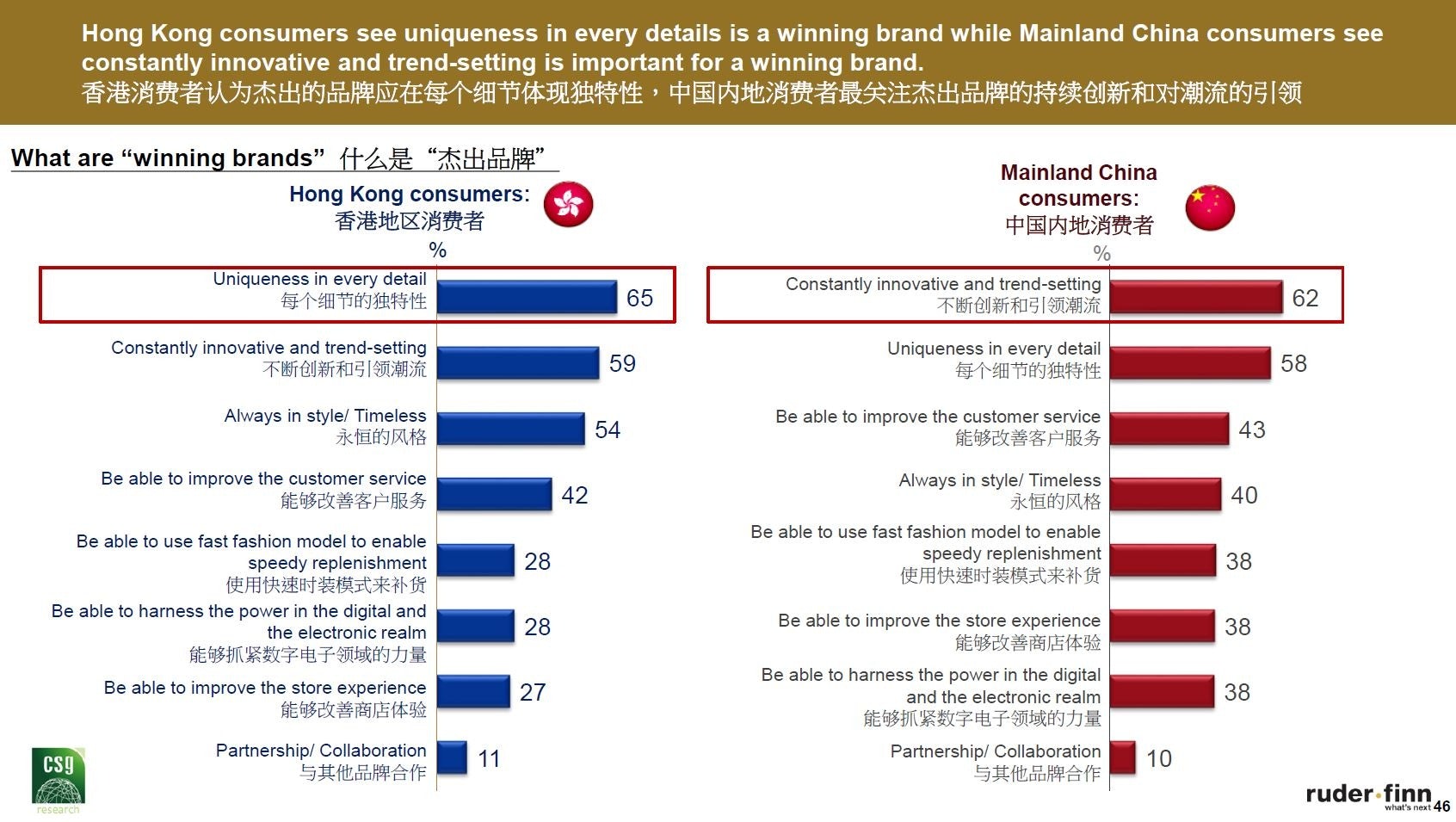

Q: In your report, mainland consumers said they value luxury brands that are constantly innovative and trend-setting. What is the implication of this to brands? In their quest to follow trends and innovate accordingly, how can they also maintain the consistency of their brand DNA?#

GM: As we said in our research findings, consumers no longer stay at the moment when they fall in love with brands. They like a brand today, and may still like that brand tomorrow, but if the brand is still the same the day after tomorrow, it is likely that consumers will lose their interests. That’s why customer loyalty is not that high these days.

The so-called innovation here that brands should push is new products and image without changing the basics, such as overall aesthetics and tone which are unique to themselves. We don’t advise [them] to follow trends blindly.

Q: Back to your list again, a “partnership/collaboration” isn’t at all an important factor in determining whether a brand is winning or not to both Hong Kong and mainland consumers. But collaborating and partnering with different brands, magazines, platforms and influencers are exactly what luxury brands are striving for today. What’s your take on that?#

GM: Based on my experience in helping our clients form collaborations and partnership, it is something that is good to have but no success is guaranteed. The two brands need to have a shared value, tone, design etc. in order to be able to collaborate. So a collaboration that can really make brands happy, consumers happy, and the industry/press happy is extremely hard. I think that’s why our consumers don’t have much expectation from it.

ST: Yes, you have to let it happen organically in terms of the collaboration that you talk about. But [collaborations with] Chinese KOLs are completely understandable. China’s KOLs are really, really smart because they are no longer just producing on their own. They’re putting themselves out there. They are saying, “You know what? I’ll co-create together with the brand.” Mr. Bags, for example, is co-creating [with] many brands, and he’s making so much money because of the co-creations. So could you call this a collaboration? Yes, it’s a collaboration. But this is something very different from two brands coming together.

Q: The report said, “Omnichannel presence is a must.” How are luxury brands in China doing in terms of forming omnichannel retail strategies?#

ST: Very, very awful! The only brand that continues to have digital as a core strategy is Burberry. All the other brands are saying, “Yes, we’ll do it,” but they’re not really doing it, I’m sorry to say. I hate to say this, but if you think about Chanel, Chanel is very popular and they should be putting a lot of items out there, but they’re not. They’re not even putting their own store out there.

GM: They still have a long way to go. To add to Sam’s point, I think there are some brands at least having some good omnichannel campaigns. They are just initial stages. They’re not taking it to the next step to apply what they have done and learned from certain campaigns to improve the overall omnichannel capabilities. If brands really want to master omnichannel retail, they have to look at it from a higher and more strategic perspective than they are right now.

Q: How likely is it for luxury brands to become omnichannel players without collaborating with Alibaba or Tencent?#

GM: In today’s environment, Alibaba and Tencent are in a monopolistic position. So not working with them is almost unrealistic.

ST: Brands can control prices, but today in China, we are seeing a lot of them cooperating. So they have to open stores on Tmall or WeChat. They have less control because you are on another platform. So what is happening right now is that we are starting to see aggregators. You see the coming of Tmall Luxury Pavilion and [JD.com] TopLife, but over there you’re still not in total control of your brand. Why? Because you’re still creating a store within this, and you know from time to time Alibaba and JD.com can decide when they want to have discounts.

GM: I think what is more important is that brands need to know their development stage in the market and how they can collaborate. And these platforms (Alibaba and Tencent) are also innovating and changing to provide a better environment for luxury brands. I think both sides need to give effort to work together.

This interview was edited and condensed. To access the full report, please visit Jing Daily's report library.