It’s clear that traditional e-commerce can no longer satisfy customers, at least not in China. The current norm of online shopping is all about human interaction: having friends, family, influencers have taken the place of trusted in-store sales associates to help customers weed out advertising noise and give personalized suggestions for faster and more effective checkouts.

The story of Pinduoduo, a mini-program that can be viewed as a marriage of Facebook and Groupon, is a good example of how successful the new concept of social commerce is becoming. The platform was built in 2015 on WeChat and follows a “the more people buy the cheaper the price” model. It was an instant success among Chinese budget shoppers, with a market valuation that jumped 10 times in one year and reached 15 billion by April 2018. And, shockingly, it’s now set to overtake the second largest e-commerce platform JD.com in gross merchandise volume by 2021, as projected by the investment bank UBS group. Even though Pinduoduo serves value-conscious consumers in underserved cities—a somewhat different demographic than the luxury market—it continues to prove the power of WeChat traffic as well as the growing popularity of social commerce.

In its latest social commerce report, the market research company Nielsen predicted even more of this growth. "In the past five years, the annual compound growth rate of social commerce has reached 100.6%, and its penetration rate has increased from 2% in 2013 to 11.9% at present and will continue to grow at a faster rate in the future," says Tommy Hong, VP of E-commerce in Nielsen China.

The reported was generated based on interviews from 3,531 online shoppers over the past 12 months. Below are two key findings brands should be aware of:

80 percent of impulsive shopping comes from social commerce#

The “social network” effect seems to offer powerful leverage for making shopping decisions. In the report, 54 percent of interviewees said they increased expenses in unplanned shopping in the past year, 80 percent of which said social recommendations like friends’ suggestions, WeChat groups, or content platforms were major channels that stimulated those impulse purchases.

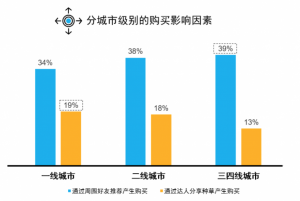

First-tier cities and lower-tier cities have different social influences#

For brands planning their social commerce budgets, they should be aware of the different preferences for first-tier and lower-tier cities, so as to match their targeted audience. People from first-tier cities are more likely to form their own social circle based on common interests and rely on influencer or KOL reviews. This is because their social circle is more diverse and their shopping choices are broader. But people in lower-tier cities rely on their acquaintances for a sense of trust when shopping online.

Social commerce may be the gateway for brands to access specific demographics, but the customer’s intent to purchase on the platform isn’t always as strong, so brands should plan their e-commerce mix wisely. Understand what the various sites contribute to in terms of inspiring, validating, or completing purchases.